Brief Matrix Algebra Review

Matrix algebra is a form of mathematics that allows

compact notation for, and mathematical

manipulation of, high-dimensional expressions and equations. For the purposes of

this

class, only a relatively simple exposition is required, in order to understand

the notation for

multivariate equations and calculations.

1 Matrix Notation

The basic unit in matrix algebra is a matrix, generally

expressed as:

(1)

(1)

Here, the matrix A is denoted as a matrix by the boldfaced type. Matrices

are also

often denoted using bold-faced type. Matrices can be of any dimension; in this

example,

the matrix is a '3-by-3'or '3 × 3'matrix. The number of

rows is listed first; the number of

columns is listed second. The subscripts of the matrix elements (a's) clarify

this: the 3rd

item in the second row is element a23. A matrix with only one element

(i.e., 1 × 1 dimension)

is called a scalar. A matrix with only a single column is called a column

vector; a matrix

with only a single row is called a row vector. The term 'vector' also has

meaning in analytic

geometry, referring to a line segment that originates at the origin (0, 0, . . .

0) and terminates

at the coordinates listed in the k dimensions. For example, you are already

familiar with the

Cartesian coordinate (4, 5), which is located 4 units from 0 in the x dimension

and 5 units

from 0 in the y dimension. The vector [4, 5], then, is the line segment formed

by taking a

straight line from (0, 0) to (4, 5).

2 Matrix Operations

The first important operation that can be performed on a

matrix (or vector) is the transpose

function, denoted as: A' or AT. The transpose function reverses the

rows and columns of a

matrix so that:

(2)

(2)

This equation says that the i, j−th element of the

transposed matrix is the j, i−th element

of the original element for all i = 1 . . . I and j = 1 . . . J elements. The

dimensionality of a

transposed matrix, therefore, is the opposite of the original matrix. For

example, if matrix

B is 3 × 2, then matrix BT will be of

dimension 2 × 3.

With this basic function developed, we can now discuss

other matrix functions, including

matrix addition, subtraction, and multiplication (including division). Matrix

addition and

subtraction are simple. Provided two matrices have the same dimensionality, the

addition

or subtraction of two matrices proceeds by simply adding and subtracting

corresponding

elements in the two matrices:

(3)

(3)

The commutative property of addition and subtraction that

holds in scalar algebra also

holds in matrix algebra: the order of addition or subtraction of matrices makes

no difference

to the outcome, so that A + B + C = C + B + A.

Matrix multiplication is slightly more difficult than

addition and subtraction, unless one

is multiplying a matrix by a scalar. In that case, the scalar is distributed to

each element in

the matrix, and multiplication is carried out element by element:

(4)

(4)

In the event two matrices are being multiplied, before

multiplying, one must make sure

the matrices 'conform' for multiplication. This means that the number of columns

in the

first matrix must equal the number of rows in the second matrix. For example,

one can not

post-multiply a 2 × 3 matrix A by another 2

× 3 matrix B , because the number of columns

in A is 3, while the number of rows in B is 2. One could however multiply

A by a 3 × 2

matrix C. The matrix that results from multiplying A and C

would have dimension 2 × 2

(same number of rows as the first matrix; same number of columns as the second

matrix).

The general rule for matrix multiplication is as follows: if one is multiplying

A × C = D,

then:

(5)

(5)

This says that the ij −th element of matrix D

is equal to the sum of the multiple of the

elements in row i of A and the column j of C . Matrix

multiplication is thus a fairly tedious

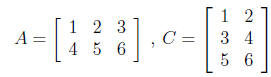

process. As an example, assume A is 2 ×3 and C

is 3 ×2, with the following elements:

(6)

(6)

Then, element d11 = (1 × 1) + (2

× 3) + (3 × 5) = 22, and the

entire D

matrix is (solve

this yourself):

(7)

(7)

Notice that D is 2 × 2.

Unlike matrix addition and subtraction, in which order of

the matrices is irrelevant, order

matters for multiplication. Obviously, given the conformability requirement,

reversing the

order of matrices may make multiplication impossible (e.g., while a 3

× 2 matrix can be

post-multiplied by a 2 × 4 matrix, the 2

× 4 matrix can NOT be post-multiplied by the 3 × 2

matrix). However, even if matrices are conformable for multiplication after

reversing their

order, the resulting matrices will not generally be identical. For example, a 1

× k row vector

multiplied by a k × 1 column vector will yield a scalar

(1?), but if we reverse the order of

multiplication, we will obtain a k × k matrix.

Some additional functions that apply to matrices and are

commonly seen include the

trace operator (the trace of A is denoted TrA), the determinant,

and the inverse. The trace

of a matrix is simply the sum of the diagonal elements of the matrix. The

determinant is

more difficult. Technically, the determinant is the sum of the signed multiples

of all the

permutations of a matrix, where 'permutations' refer to the unique combinations

of a single

element from each row and column, for all rows and columns. If d denotes the

dimensionality

of a matrix, then there are d! permutations for the matrix. For instance, in a 3

× 3 matrix,

there are a total of 6 permutations (3! = 3 × 2

×1 = 6): (a11, a22, a33),

(a12, a23, a31), (a13,

a21, a32), (a13, a22, a31),

(a11, a23, a32), (a12, a21,

a33). Notice how for each combination, there

is one element from each row and column. The signing of each permutation is

determined

by the column position of each element in all the pairs that can be constructed

using the

elements of the permutation, and the subscript of element at each position in

each pair.

For example, the permutation (a11, a22, a33)

has elements from columns 1,2, and 3. The

possible ordered (i, j) pairs that can come from this permutation include (1,

2), (1, 3), and

(2, 3) (based on the column position). If there are an even number of (i, j)

pairs in which

i > j, then the permutation is considered even and takes a positive sign;

otherwise, the

permutation is considered odd and takes a negative sign. In this example, there

are 0 pairs

in which i > j, so the permutation is even (0 is even). However, in the

permutation (a13,

a22, a31), the pairs are (3, 2), (3, 1), and (2, 1). In

this set, all three pairs are such that i > j,

hence this permutation is odd and takes a negative sign. The determinant is

denoted using

absolute value bars on either side of the matrix name: for instance, the

determinant of A is

denoted as |A|.

For 2 × 2 and 3 ×

3 matrices, determinants can be calculated fairly easily; however, for

larger matrices, the number of permutations becomes large rapidly. Fortunately,

several

rules simplify the process. First, if any row or column in a matrix is a vector

of 0, then the

determinant is 0. In that case, the matrix is said not to be 'of full rank'.

Second, the same

is true if any two rows or columns is identical. Third, for a diagonal matrix

(i.e., there are

0s everywhere but the main diagonal-the 11, 22, 33,... positions), the

determinant is only

the multiple of the diagonal elements. There are additional rules, but they are

not necessary

for this brief introduction. We will note that the determinant is essentially a

measure of the

area/volume/hypervolume bounded by the vectors of the matrix. This helps, we

think, to

clarify why matrices with 0 vectors in them have determinant 0: just as in two

dimensions

a line has no area, when we have a 0 vector in a matrix, the dimensionality of

the figure

bounded by the matrix is reduced by a dimension (because one vector doesn't pass

the

origin), and hence the hypervolume is necessarily 0.

Finally, a very important function for matrix algebra is

the inverse function. The inverse

function allows the matrix equivalent of division. In a sense, just as 5 times

its inverse

1/5 = 1, a matrix A times its inverse-denoted A-1-equals I, where I

is the 'identity

matrix'. A

n identity matrix is a diagonal matrix with ones along the

diagonal. It is the matrix

equivalent of unity (1). Some simple algebraic rules follow from the discussion

of inverses

and the identity matrix:

AA-1 = A-1A = I (8)

Furthermore,

AI = IA = A (9)

Given the commutability implicit in the above rules, it

stands that inverses only exist

for square matrices, and that all identity matrices are square matrices. For

that matter, the

determinant function can only apply to square matrices also.

Computing the inverse of matrices is a difficult task, and

there are several methods by

which to derive them. Probably the simplest method to compute an inverse is to

use the

following formula:

(10)

(10)

The only new element in this formula is the adj A , which

means 'adjoint of A

.' The

adjoint of a matrix is the transpose of its matrix of cofactors, where a

cofactor is the signed

determinant of the 'minor' of an element of a matrix. The minor of element i, j

can be found

by deleting the ith row and jth column of the matrix. For example,

the minor of element

a11 of the matrix A above is:

(11)

(11)

Taking its determinant leaves one with a scalar that is

then signed (by multiplying by

−1i+j). In this case, we obtain (−1)2(a22a33

−a23a32) as the cofactor for element a11. If

one

replaces every element in matrix A with its signed cofactor, then

transposes the result, one

will obtain the adjoint of A . Multiplying this by 1/|A| (a scalar) will

yield the inverse of

A .

There are a number of important properties of cofactors that enable more rapid

computation

of determinants, but discussing these is beyond the scope of this simple

introduction.

Fortunately, computer packages tend to have determinant

and inversion routines built

into them, and there are plenty of inversion algorithms available if you are

designing your

own software, so that we generally need not worry. It is worth mentioning that

if a matrix

has a 0 determinant, it does not have an inverse. There are many additional

matrix algebra

rules and tricks that one may need to know; however, they are also beyond the

scope of this

introduction.

3 The OLS Regression Solution in Matrix Form

We close this section by demonstrating the utility of

matrix algebra in a statistical problem:

the OLS regression solution.

When dealing with the OLS regression problem, we

can think of the entire data set in

matrix terms:

(12)

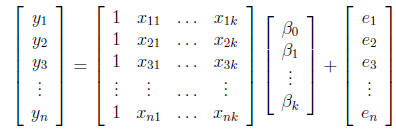

(12)

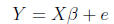

In this problem, there are n individuals in the dataset measured on one

dependent (outcome)

variable y, with k regressor (predictor) variables x, and hence k coefficients

to be

estimated. The column of ones represents the intercept. If one performs the

matrix algebra

(multiplication) for the first observation, y1, one can see that:

(13)

(13)

which is exactly as it should be: the dependent variable

for observation 1 is a linear

combination of the individual's values on the regressors weighted by the

regression coefficients,

plus an individual-specific error term. This equation can be written more

succinctly

by simply writing:

(14)

(14)

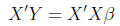

How can we solve for  ? Just as in scalar algebra, we need

to isolate

? Just as in scalar algebra, we need

to isolate  . Unlike scalar

. Unlike scalar

algebra, however, we can't simply subtract the error term from both sides and

divide by X,

because a) there is no matrix division, really, and b) multiplication must

conform. So, we

first multiply both sides by

(15)

(15)

We multiply by the transpose of X here, because X-1Y

would not conform for multiplication.

One of the assumptions of OLS regression says that X and e are

uncorrelated, hence

Thus, we are left with:

Thus, we are left with:

(16)

(16)

From here, we need to eliminate

from the right side of the equation. We can

do

from the right side of the equation. We can

do

this if we take the inverse of

and multiply both sides of the equation by

it:

and multiply both sides of the equation by

it:

(17)

(17)

This follows, because A-1A = I and IA = A.

Thus, the

OLS solution for  is

is

which should look familiar.

which should look familiar.